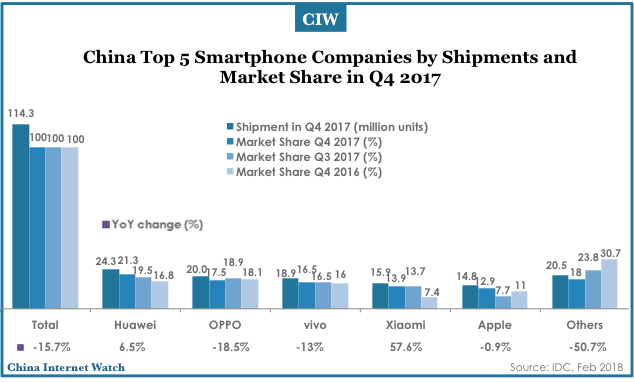

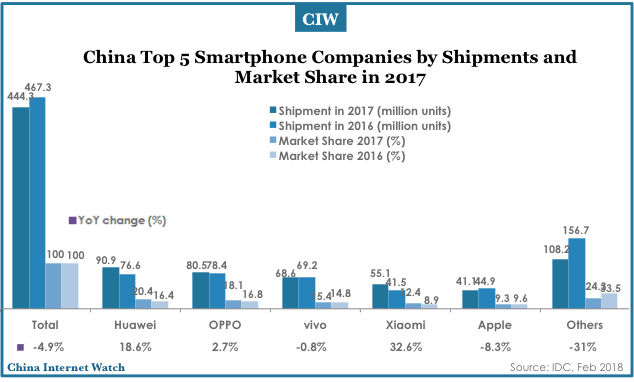

China smartphone market declined 15.7% year-over-year (YoY) in Q4 2017 and 4.9% for the whole of 2017 according to IDC.

Apple’s share increased YoY and QoQ in Q4 2017. Although the iPhone X was available in short supply initially at launch in early November 2017, the supply constraints for this model eased towards the end of the quarter. Apple’s ASP increased by 23.9% YoY in 2017Q4 largely due to the shipments of the iPhone X. Apple alone made up 85% of the overall shipments in >US$600 premium segment.

Huawei appears on the radar to compete with Apple in the >US$600 premium segment. Huawei grew in Q4 2017 largely due to the strong shipment for both its Honor and Huawei branded phones in the

With Samsung’s continued troubles in the China market, Huawei has successfully managed to break into the high-end Android vendor space, although price points of the flagship Huawei phones are carefully priced lower than the iPhone prices at launch.

OPPO and vivo are focusing more on the mid-range segment, with a higher share of their portfolio focused on the mid-range segment compared to a year ago. The reduction in the number of OPPO and vivo models in the low-end segment also contributed to their YoY decline in Q4 2017.

While focusing more on the mid-range segment has hurt its overall shipment growth, OPPO and Vivo’s overall ASPs have increased YoY. In terms of revenue, OPPO ranked second to Apple and was above Huawei. vivo follows at fourth place. Thus, while OPPO’s shipments may have declined, it is growing in terms of its overall revenue.